International Tax Forms

New Internal Revenue Service (IRS) guidelines regarding the Foreign Account Tax Compliance Act (FATCA) went into effect July 1, 2014.

FATCA requires payors such as NC State to:

- Have procedures in place to identify withholdable payments and categorize non-US payees.

- Have procedures in place to report and potentially apply withholding tax to avoid liability and exposure to potential penalties.

- To verify the payee’s FATCA status with the receipt of appropriate documentation (the correct W-9 or W-8 form).

The US Department of the Treasury’s Office of Foreign Assets Control (OFAC) prohibits payments to any person or entity that has been added to any of our government’s sanction lists. Without receiving the appropriate legal form, NC State cannot meet IRS’s FATCA requirements for each payee.

According to the IRS, the University as a withholding agent must request a W-8 form from ANY individual or entity that is presumed to be a foreign person. Request a form W-8 form before you make a payment to someone who you believe to be a foreign person. International vendors must submit a US withholding certificate (W-8 series of forms) with an Employer Identification Number (EIN ), or Individual Taxpayer Identification Number (ITIN), or Social Security Number (SSN) in order to claim an exemption from or reduction in withholding. With regards to business payments, the EIN, ITIN or SSN can only be used by the vendor for US business tax obligations and cannot be used for US personal tax obligations.

The specific W-8 form used by the international vendor depends on:

– type of payment being paid, and

– status of the business itself.

- W-8BEN

- W-8BEN-E NCSU-Substitute form, Certificate of Foreign Status Non-FATCA (Entities Only-Short Form)

- W-8BEN-E Substitute Form TEMPLATE, Non-FATCA (Example for departments and vendors)

- W-8BEN-E Long Form

- W-8BEN-E Checklist for completing the form

- W-8ECI

- W-8IMY

- W-8EXP

{kind=link}

International Suppliers Tax FAQs

W-8BEN: The W-8BEN is used to confirm that a vendor is an individual foreign person (not a company) and must be provided even if the vendor is not claiming a tax treaty reduction or exemption from withholding. Therefore, all foreign vendors must provide a W-8BEN even if no EIN, ITIN or SSN exists, unless another W-8 series form is provided. A valid W-8BEN must be provided before payment is issued by NCSU.

A W-8BEN that doesn’t have an ITIN, EIN or SSN is valid for three calendar years following the date it is signed, unless a change in circumstances makes any of the information on the form incorrect. For example, a W-8BEN signed on October 1, 2022, without an ITIN, EIN or SSN remains valid through December 31, 2025. (Calendar Year #1 is 2023; Calendar Year #2 is 2024, and Calendar Year #3 is 2025).

A W-8BEN that does have an ITIN, EIN or SSN remains in effect until a change in circumstances makes any information on the form incorrect, provided that NC State issues at least one payment to the vendor per calendar year that is reportable on Form 1042-S. For example, an international vendor who submits a W-8BEN with a valid EIN and requests tax treaty benefits, will not have to re-submit the W-8BEN as long as NC State applies tax treaty benefits to at least one payment to the vendor each calendar year (and reports on Form 1042-S).

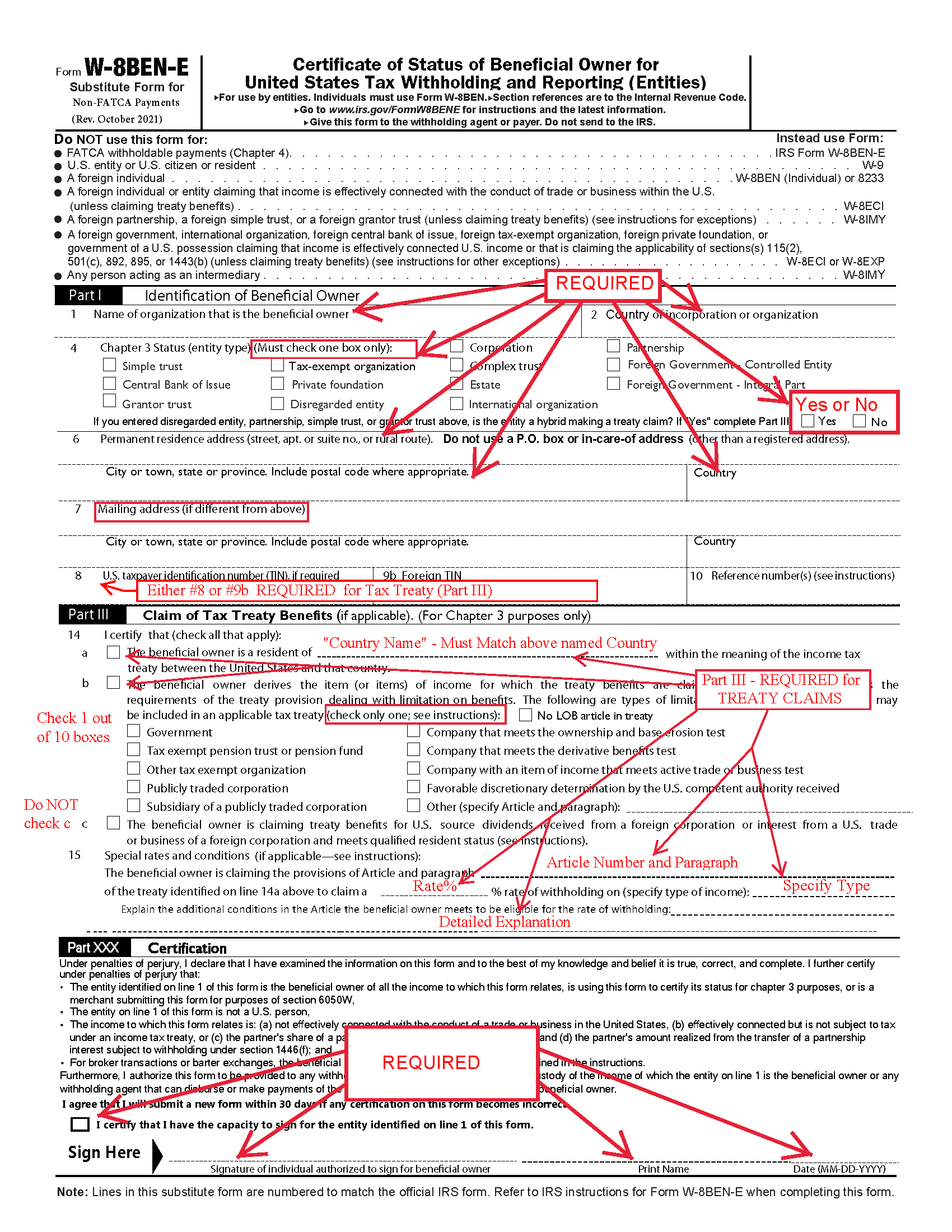

W-8BEN-E: The W-8BEN-E is used primarily by foreign entities (FE) (Partnership, corporation, company, or association). This is a new form that is a direct result of the Foreign Account Tax Compliance Act (FATCA). The W-8BEN-E is only to be filled out by entities, not individuals.

- The W-8BEN-E (Long form) contains 30 parts, and very few of them have to be filled out by particular entities. However, all foreign beneficial owners must complete Parts I (Identification of Beneficial Owner) and XXIX (Certification).

- A W-8BEN-E Substitute form for Non-FATCA payments, (one page) is also available for which the majority of the University’s payments are processed.

A letter to help International vendors fill out the W-8BEN-E follows – NC State W-8BEN-E Request

W-8ECI: The income is effectively connected with a trade or business in the U.S.A. and the owner has an EIN, ITIN, or SSN. A valid W-8ECI must be provided before payment is issued by NC State.

W-8IMY: Used by foreign intermediaries, a withholding foreign partnership, a withholding foreign trust, or a flow-through entity. The vendor has a qualified intermediary agreement with the IRS to accept primary responsibility for withholding.

W-8EXP: The beneficial owner of the payment is a tax-exempt organization under U.S. tax rules allowing the beneficial owner a claim to a reduced rate of, or exemption from, withholding as a foreign government, international organization, foreign central bank of issue, foreign tax-exempt organization, foreign private foundation, or government of a U.S. possession.